{kind=link}

Picture supply: Getty Photographs

Inventory market sentiment has shifted in the direction of worth shares in 2026. However the huge query is whether or not this rotation is a short-term problem or one thing buyers ought to take note of?

The brief reply is that it relies upon: the good cash (that’s, institutional buyers who’re controlling enormous quantities of cash) says worth shares are going to outperform over the subsequent 12 months, however the long-term image appears fairly totally different.

Good cash

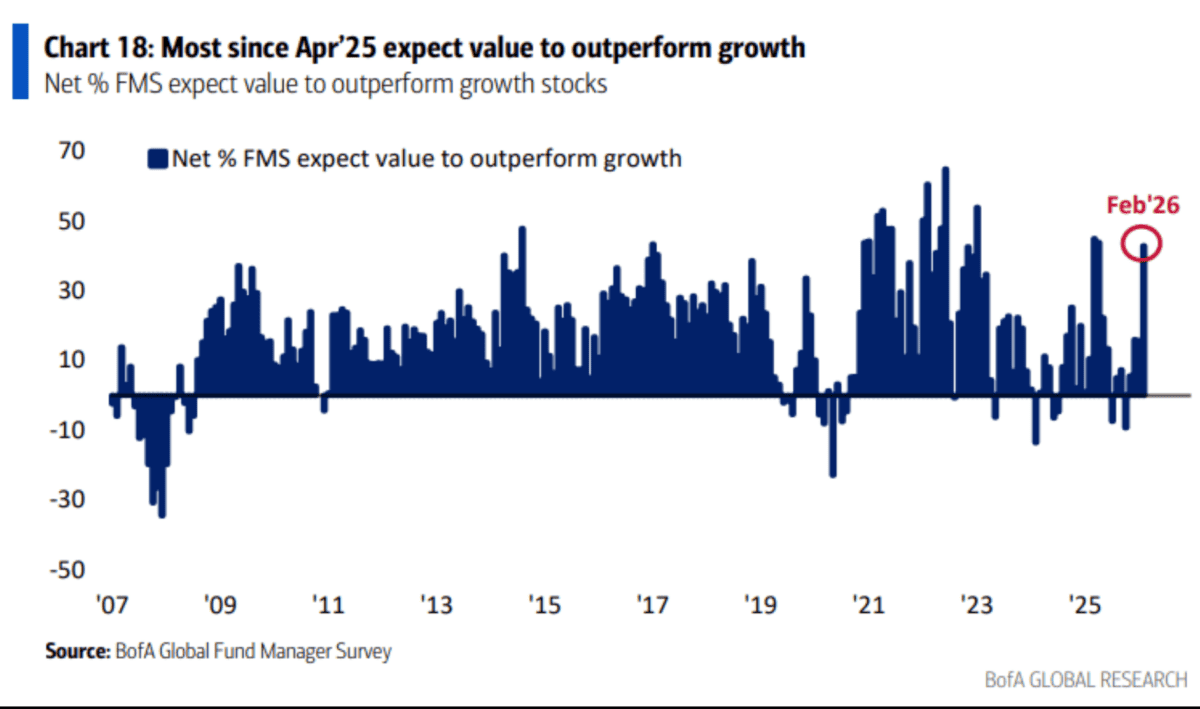

In response to the newest information from Financial institution of America, 43% of fund managers anticipate worth to be the profitable theme for the subsequent 12 months. Which may not sound like loads, however it’s.

It’s been uncommon lately to search out the good cash expressing that sort of bullish sentiment on worth shares relative to progress shares. But it surely’s the place we’re proper now.

Traders would possibly take this as their cue to begin in search of worth alternatives. And whereas I don’t assume it is a dangerous concept in any respect, there are some issues to be cautious of.

One is that sentiment can change instantly – the subsequent survey would possibly present a really totally different view. The opposite is that, traditionally, worth outperformance tends to be comparatively short-lived.

Lengthy-term investing

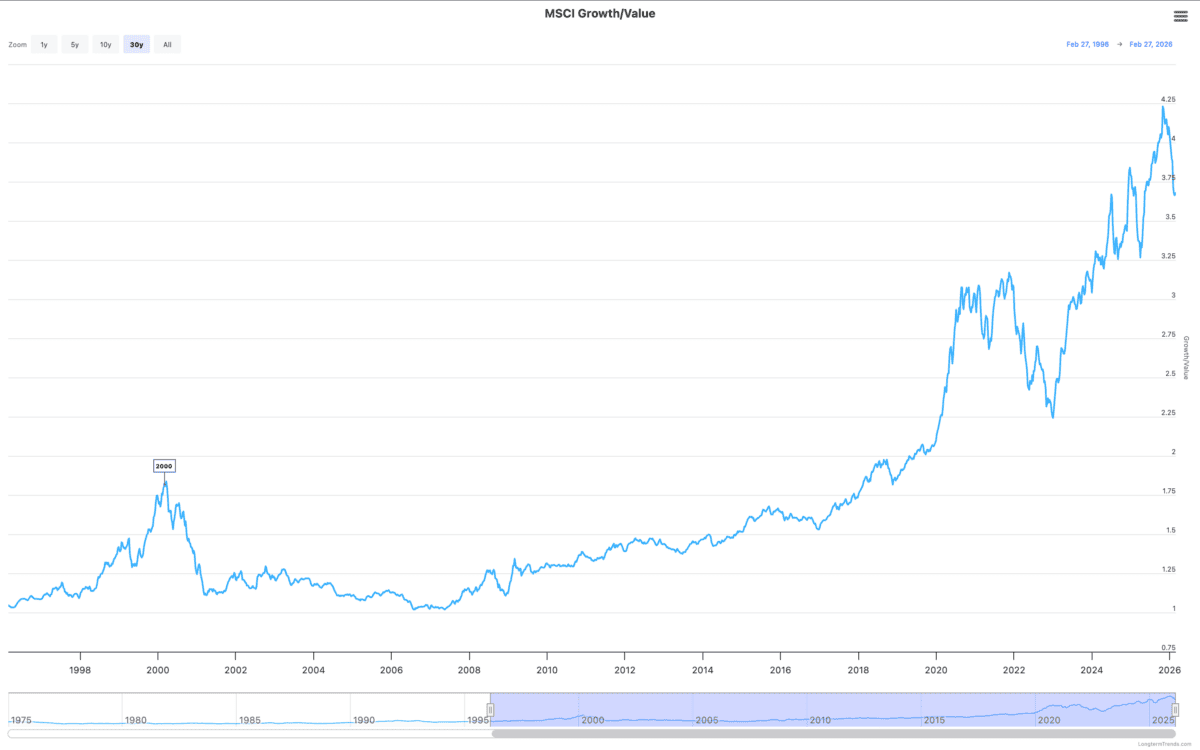

For the reason that begin of the 12 months, worth shares have crushed their progress counterparts. However from a 30-year perspective, this barely registers on what has been a sturdy development the opposite method.

The overall form of issues is that the inventory market goes in cycles. Progress shares do properly till their future earnings come into query, at which level worth shares come to the fore.

This occurred throughout the dotcom crash and on the finish of the Covid-19 pandemic. And it appears prefer it’s occurring once more as buyers strive to determine synthetic intelligence (AI).

In every case, progress shares went on to outperform. So whereas the market would possibly justifiably be fearful about datacentre spending, focusing solely on worth shares is dangerous.

A inventory I’m shopping for

Amazon‘s (NASDAQ:AMZN) the king of the large spenders proper now. In equity although, the $200bn it plans to spend is much like Microsoft as a a number of of Cloud revenues.

The stakes are excessive, however the potential rewards are enormous. Amazon’s making good progress in growing its personal Trainium chips that compete favourably with Nvidia’s newest GPUs.

That could possibly be massively worthwhile sooner or later when AI shifts from coaching to inferencing. However to actually fly, Amazon wants customers to hitch AWS over the likes of Azure or Google Cloud.

Traders although, are specializing in dangers, which is why the inventory’s unusually low cost proper now. And I’m wanting to make use of this as an opportunity so as to add to my present funding.

Progress and worth

In my very own portfolio, I don’t actually look to take care of a steadiness between totally different investing kinds. As an alternative, I attempt to concentrate on no matter the most effective alternative I can discover at any second.

That’s the results of serious about each an organization’s progress prospects and the valuation multiples it’s buying and selling at. And plenty of the time, that factors me in the direction of worth shares.

The good cash’s worth for the subsequent 12 months. However I feel the long-term prospects for progress shares are unusually good proper now, in order that’s the place I’m focusing.