{kind=link}

Picture supply: Rolls-Royce Holdings plc

Rolls-Royce (LSE:RR.) shares have been standout performers amongst FTSE 100 shares in 2023. Having risen by an astonishing 144% in lower than a yr, potential traders may be forgiven for asking themselves whether or not the Rolls-Royce share value is now relatively costly.

But, regardless of buying and selling close to a 52-week excessive, the inventory remains to be down 17% from the place it was 5 years in the past. Lengthy-term shareholders will hope the aerospace and defence big’s post-pandemic restoration has additional to run. In spite of everything, at £2.41 at this time, the share value remains to be properly beneath the all-time excessive of £4.42 it reached again in 2014.

So, let’s take a better take a look at the Rolls-Royce’s funding prospects at this time.

Valuation

First, it is sensible to deal with the topic of valuation head on.

For the reason that firm generates practically 47% of its income from delivering and sustaining civil plane, it suffered enormously within the pandemic on account of strict journey restrictions. Throughout this era, Rolls-Royce was a loss-making enterprise.

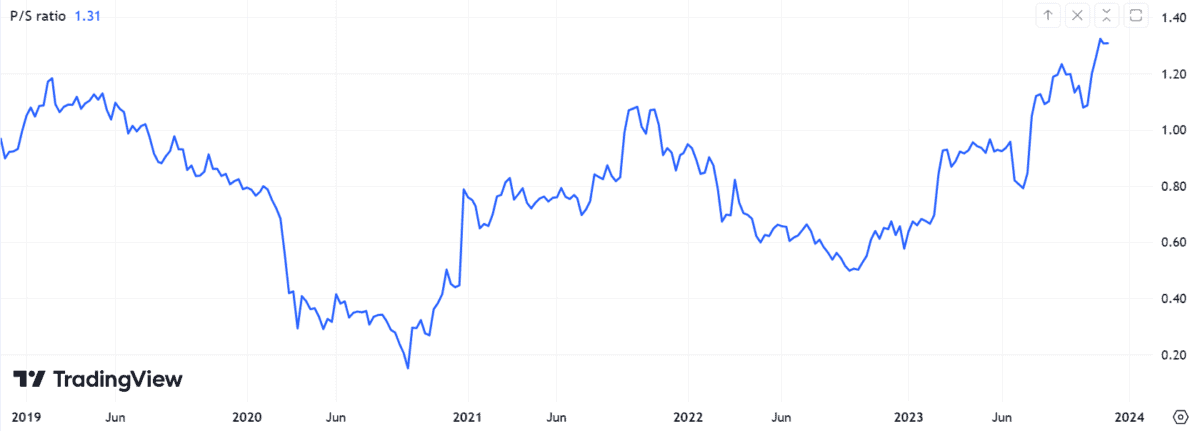

Subsequently, I imagine it’s extra enlightening to take a look at the agency’s price-to-sales (P/S) ratio, relatively than the extra broadly used price-to-earnings (P/E) ratio, to gauge its valuation at this time.

Because the chart above reveals, Rolls-Royce shares are at the moment dearer, in response to this metric, than they’ve been at any level within the final 5 years.

Consequently, worth traders could have legit considerations that the corporate will battle to generate comparable returns in 2024 in comparison with the final 12 months.

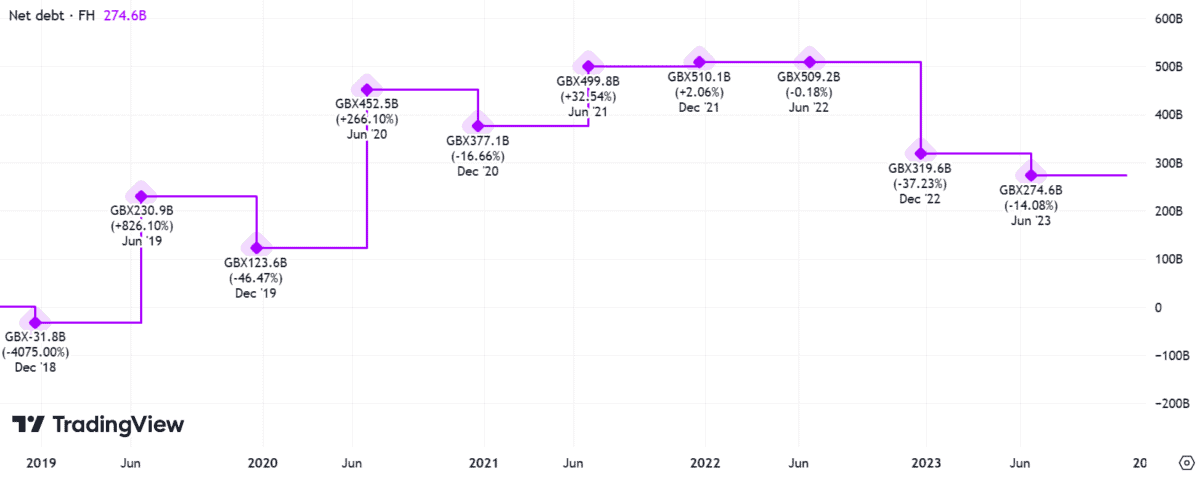

Web debt

Turning to the steadiness sheet, Rolls-Royce has made good progress in lowering the debt mountain it constructed through the pandemic. In H1 2023, this determine improved to £2.75bn, having ballooned to £5.1bn by the top of 2021.

All the main credit standing businesses now have a optimistic outlook on Rolls-Royce. That stated, the group has but to return to an investment-grade score.

| Company | Credit score Ranking |

|---|---|

| Moody’s | Ba3 |

| Fitch | BB- |

| S&P | BB |

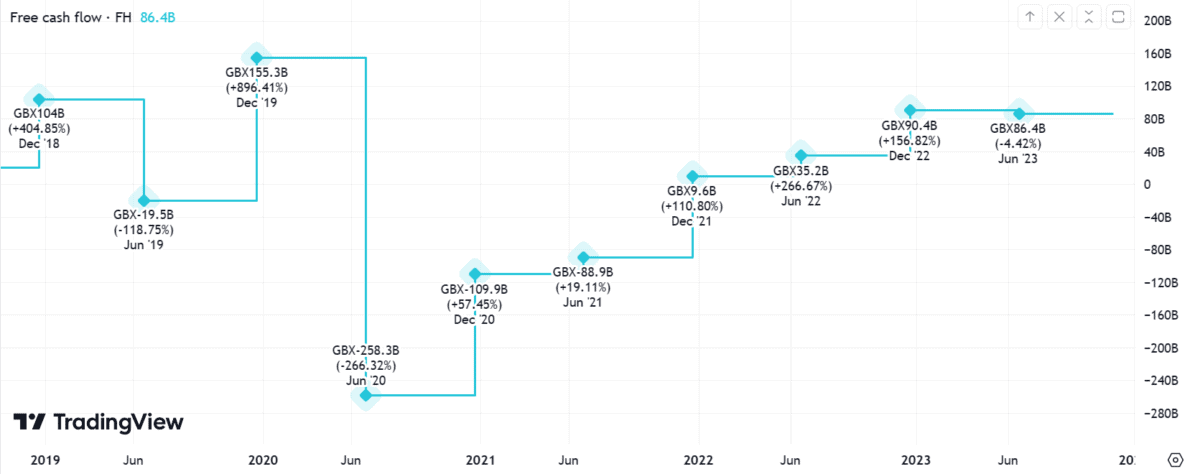

Free money circulation

I’d prefer to see the corporate generate stronger money flows over the approaching years, because it has solely not too long ago stemmed its outflows — however the trajectory appears encouraging. This may translate into score upgrades down the road.

CEO Tufan Erginbilgic has acknowledged the corporate was sluggish to reply to the inflationary setting with value hikes for its companies.

This might bode properly for future money circulation enhancements. Rolls-Royce arguably has headroom to capitalise on its aggressive benefits in elevating costs additional.

Profitability

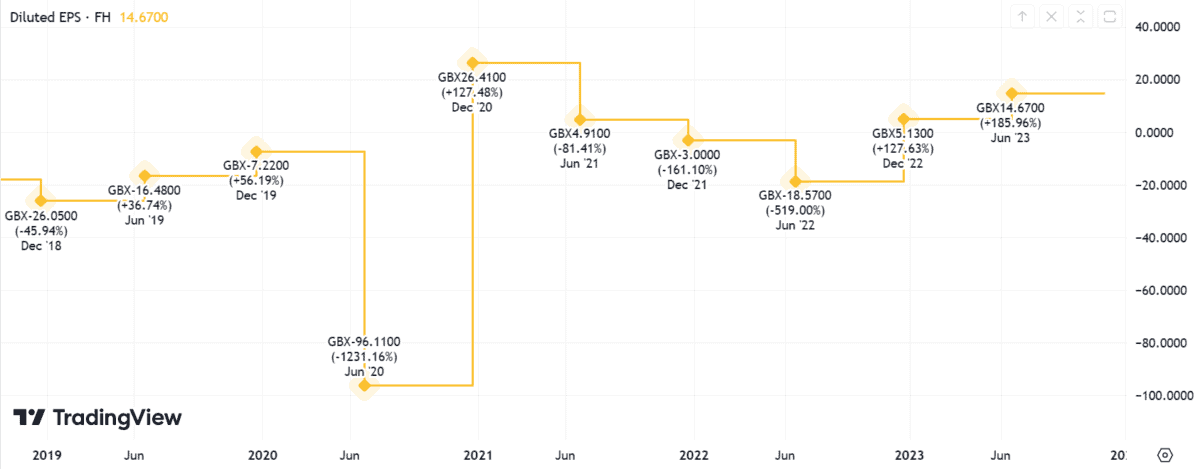

Lastly, diluted earnings per share (EPS) are practically again to the place they have been pre-Covid.

This important profitability metric is the determine that basically catches my eye. It tells the story of Rolls-Royce’s exceptional turnaround beneath Erginbilgic’s management.

A inventory to purchase?

It’s honest to say development within the Rolls-Royce share value over the previous yr has been nothing in need of spectacular.

A continued restoration in civil aviation flying hours, profitable submarine offers flowing from the AUKUS defence pact, and ground-breaking know-how for small modular nuclear reactors all add weight to the funding case.

Nonetheless, the inventory isn’t as low-cost because it was. Buyers may be smart to restrict their expectations if getting into positions at this time. Nonetheless, I’m a shareholder and can proceed to carry my place with the prospect of potential dividend reinstatements on the close to horizon.