{kind=link}

Picture supply: Getty Photographs

As a long-time holder of Persimmon (LSE:PSN) shares — I first took a place earlier than the pandemic — I’m sitting on a big loss. Since then, Covid-19, hovering inflation, rising rates of interest and a squeeze on disposable incomes have severely impacted the FTSE 100 housebuilder.

In 2022, the group offered 14,868 houses. In the present day (13 August), it launched its outcomes for the six months ended 30 June 2025 (H1 25) and reiterated its goal to construct 11,000-11,500 this yr.

Extra considerably, it reported an underlying working margin throughout H1 of 13.1%. In 2022, it was over 30%.

Not surprisingly, the group’s share value has fallen 56% since August 2020.

My dilemma

Towards this backdrop, I recurrently replicate on Warren Buffett’s well-known quote.

The American billionaire as soon as mentioned: “Ought to you end up in a chronically leaking boat, vitality dedicated to altering vessels is prone to be extra productive than vitality dedicated to patching leaks.”

Nevertheless, I feel the leaks in Persimmon’s boat are slowly being repaired. And the ocean through which it sails (the broader {industry}) seems to be to be much less tough than beforehand.

Some inexperienced shoots

In the present day’s outcomes revealed that, in comparison with the primary half of 2024, new housing income was 12% greater and working revenue was up 13%. The group’s order guide is £1.25bn – an 11% improve on a yr in the past. And it expects a full-year margin of 14.2%-14.5% with additional enchancment in 2026. Subsequent yr, it hopes to finish 12,000 properties.

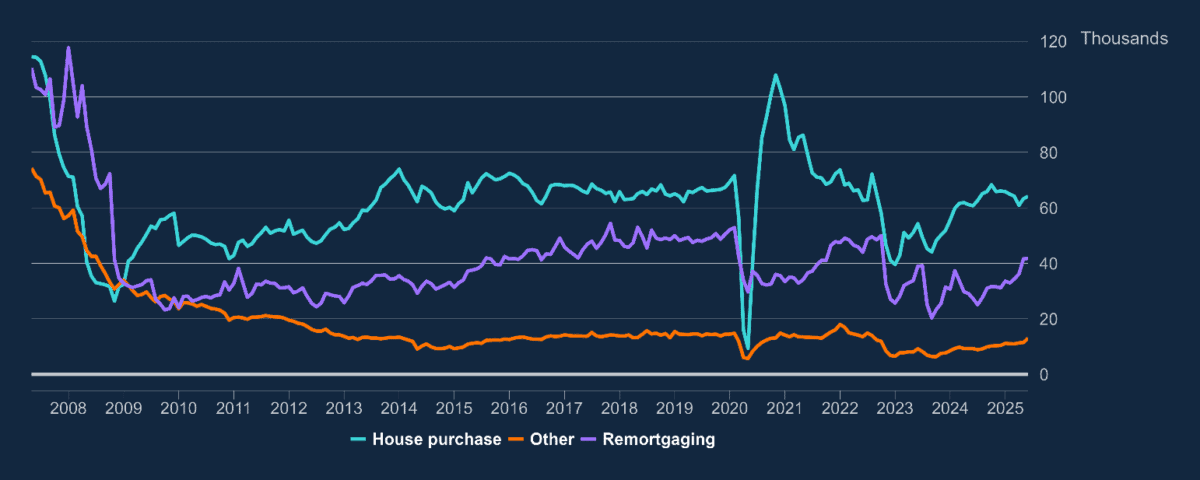

Wanting on the UK housing market as an entire, persistent inflation means rates of interest might not be falling as rapidly as hoped (or beforehand anticipated) however the route of journey is for cheaper borrowing prices. Figures from the Financial institution of England present that the precise quantity paid on loans drawn in June was 4.34% versus 4.47% in Might. This has now fallen for 4 consecutive months.

Mortgage lending statistics have been distorted in March by a rush of first-time patrons seeking to purchase properties earlier than modifications in stamp responsibility charges took impact. Nevertheless, the annual development fee in web mortgage lending elevated from 2.4% in Might to 2.6% in June. In comparison with a yr earlier, there have been 23% extra mortgage approvals in the course of the month.

Future prospects

Understandably given the turbulence of the previous 5 years, Persimmon stays cautious. It says: “As we glance forward, the tempo of margin development can be impacted by diminishing embedded construct price inflation, on-going affordability constraints and elevated industry-wide prices. Nevertheless, with a steady housing market, we stay assured of additional development in retailers, quantity and revenue.”

However I stay optimistic in regards to the long-term prospects for the UK’s housebuilders. There’s already a scarcity of housing and the state of affairs’s predicted to worsen. Persimmon sells cheaper houses than its FTSE 100 rivals, which suggests it may return to earlier ranges of housebuilding extra rapidly. Within the housing market, the demand for cheaper properties tends to rebound sooner.

I subsequently plan to carry on to my shares. And for a similar causes, different traders may think about taking a place. They may additionally get themselves a inventory that’s now yielding 5.4%. This places it within the prime fifth of Footsie dividend payers. Though payouts are by no means assured, I feel there’s sufficient optimistic information in Persimmon’s interim outcomes to recommend that the dividend’s safe for now.