{kind=link}

Picture supply: Getty Pictures

Tesco (LSE:TSCO) shares rose by simply 1% on Wednesday 8 April. In the meantime, Marks & Spencer was up almost 7%.

So, what’s taking place? Let’s discover.

It was by no means crushed up

When the battle began within the Gulf, markets fell. However it wasn’t equal. In reality, some shares gained, akin to oil and delivery.

Tesco wasn’t a gainer, however buyers had been slower to promote their shares within the FTSE 100 grocer. And that’s all resulting from threat.

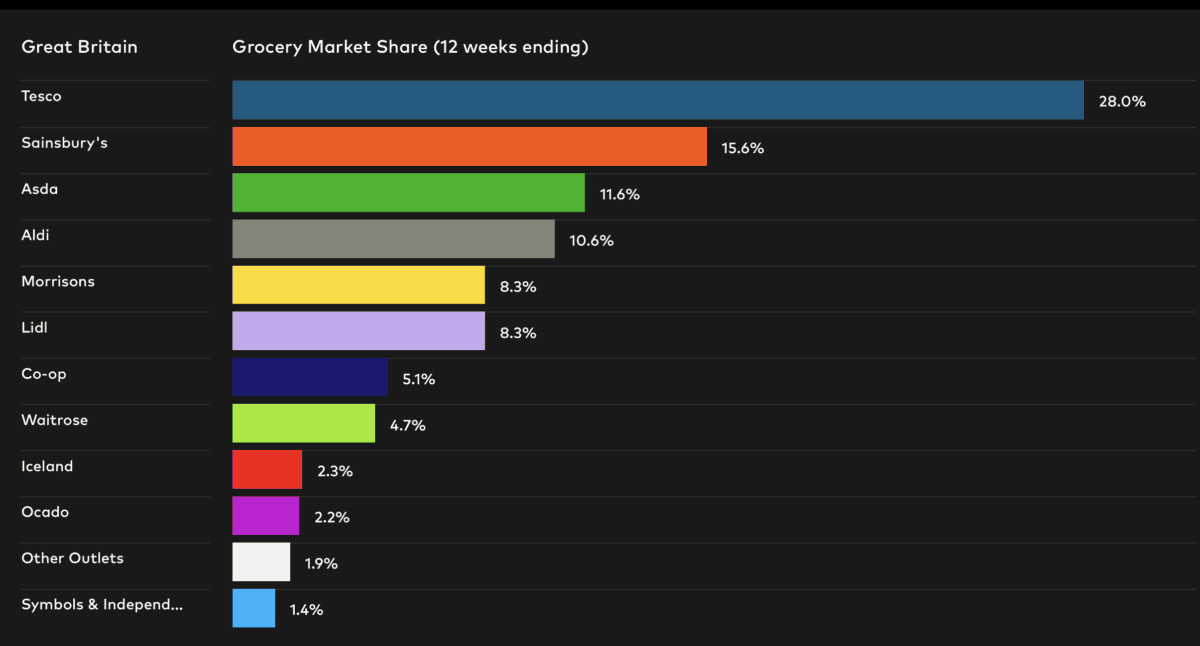

Tesco sells groceries. Folks purchased them earlier than the struggle, throughout it, and so they’ll maintain shopping for them now. That predictability makes it what fund managers name a defensive inventory — one with low sensitivity to the financial cycle. When the world turns unsure, cash tends to circulate in direction of shares like Tesco moderately than away from them. It’s not thrilling, however it’s dependable.

That dynamic protected Tesco on the best way down. The identical dynamic is working in opposition to it immediately. The ceasefire is a risk-on occasion — buyers are pouring again into the shares that offered off hardest: banks, airways, housebuilders. Tesco didn’t unload onerous, so it doesn’t snap again onerous. You may’t get better floor you by no means misplaced.

In follow there’s some extra nuance right here. Tesco has larger cost-efficiencies than its friends and within the occasion of sustained price inflation, clients might commerce down from Marks & Spencer to friends like Tesco.

Nevertheless, larger oil and power costs undoubtedly damage the grocery store big. It has a logistics fleet, deliveries, and fridges to run.

Buying and selling very near honest worth

Tesco is a British champion. It’s an operational masterpiece and the model power is just about unmatched. It has additionally confirmed its capability to combat off competitors from friends like Lidl and Aldi. Due to this, it deserves to commerce at one thing of a premium to its friends.

It’s additionally a phenomenally constant performer. Income has grown in yearly for the reason that pandemic and it’s forecasted to do the identical in 2026 and 2027.

Nevertheless, the issue is realizing how large that premium must be. Tesco is at the moment buying and selling round 15.3 instances ahead earnings, presents a 3.3% dividend yield — coated 1.99 instances by earnings — and has £10.3bn in web debt — that’s round 11 instances web revenue.

On the different finish of the dimensions, there’s Marks & Spencer. It trades a ten.3 instances ahead earnings, presents a 1.96% dividend yield — coated 5.04 instances by earnings — and carries a web debt place of £2.5bn — that’s round 6 instances web revenue.

My take

Tesco is an unbelievable firm. Nevertheless, I’m beginning to assume that the premium is a bit stretched. Institutional analysts agree with the inventory buying and selling simply 1% above the present worth. It’d nonetheless be price contemplating, however I believe there’s positively higher worth to be discovered elsewhere.