{kind=link}

Picture supply: Getty Photos

I’m researching penny shares and Metals Exploration (LSE:MTL) is a UK-based firm that’s risen 154% over the previous yr, climbing from 1.6p to 4p since final March.

The £85m mining firm identifies and extracts valuable metals and base metallic deposits within the Philippines. Headquartered in London and working since 2004, the corporate has been struggling to succeed in the highs it loved within the early days.

Again in 2006, the share value climbed as excessive as 47p. The next years had been very unstable however by 2013 it had fallen under 10p and by 2019 it was below 1p.

A turning tide

The corporate just lately finalised a share buy settlement that would flip its fortunes round. The acquisition would give it a controlling share of Yamang Mineral Company (YMC), a agency that holds prospecting rights to the 16,000ha gold-rich Cordillera space of the Philippines.

Mining is predicted to start within the second half of 2024 pending agreements with native communities and preliminary exploration efforts.

“If we now have the exploration success we’re focusing on, we purpose to give attention to growing a high-grade, smaller-scale gold production-ready mission as quickly as doable,” mentioned interim chairman Steven Smith.

The share value has been rising steadily since information of the settlement first surfaced in late January. It’s now at its highest degree in seven years and is predicted to proceed climbing.

Financials

Impartial analysts estimate Steel Exploration shares to be undervalued by as a lot as 76%. That is seemingly based mostly on the corporate’s spectacular efficiency thus far, with earnings rising at an annual fee of 68% — seven occasions the trade common.

That’s helped push its revenue margins to twenty-eight.7%, up from 4.9% final yr. Utilizing a reduced money movement mannequin, we are able to see that the undervaluation thesis is supported by a forward-looking price-to-earnings (P/E) ratio of two.4 occasions.

However development like that comes at a value.

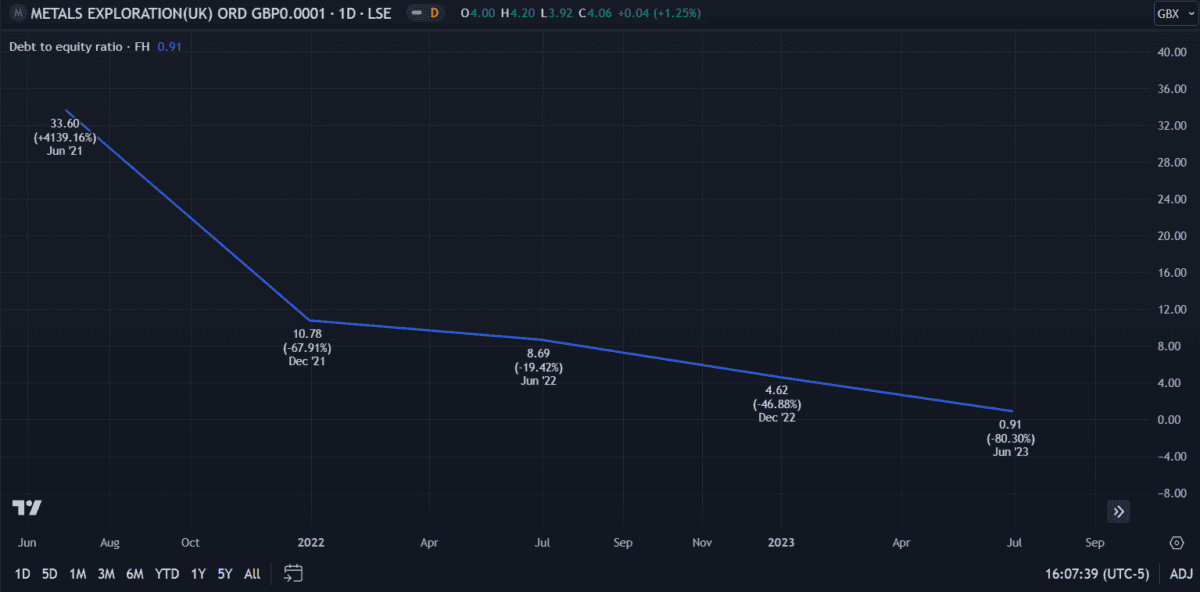

Metals Exploration has spent the previous few years climbing out of a deep debt gap. Solely just lately did its debt-to-equity (D/E) ratio drop under 1, placing it in a steady place.

Again in June 2021, the corporate was drowning in debt 33.6 occasions increased than its fairness. It now holds £54.2m in fairness and solely £49.3m in debt. That’s a formidable turnaround — though nonetheless dangerous because it’s a reasonably excessive degree of debt for an £85m firm.

Gold demand

To guage a enterprise’s future prospects we have to take into account demand for its merchandise. Wanting on the broader gold mining trade, demand has remained comparatively steady over the previous 10 years, barring a minor dip in 2020 throughout Covid.

Gold is among the most valuable metals on this planet – considered the primary metallic found by people. With such an extended historical past, it’s unlikely demand will cut back within the close to future. Ought to Metals Exploration proceed to safe precious gold deposits, it will likely be in an excellent place to profit from this trade.

Present forecasts nonetheless anticipate income and earnings to say no by 11.4% and 23.6% per yr, respectively. Nevertheless, if the brand new Cordillera mine proves worthwhile, I anticipate these figures to show optimistic.

For now, I’m placing Metals Exploration on my penny inventory watchlist with the intent to purchase if the forecast improves.