{kind=link}

Picture supply: Getty Photos

Rolls-Royce (LSE:RR) shares motored to a brand new file on the finish of final month, reaching an intraday excessive of 1,420p. This adopted the FTSE 100 engine maker’s full-year 2025 outcomes, which had been glorious.

Two days later nevertheless, the US and Israel started bombing Iran, sending the FTSE 100 down sharply. The Rolls-Royce share worth has now pulled again to 1,292p, as I sort, a fall of round 9% from its excessive.

I’ve been ready for a dip to think about shopping for extra shares. Is that this the chance I’ve been ready for?

The platform’s burning no extra

It’s no secret that Rolls-Royce inventory has been a mind-bogglingly good funding in recent times. The truth is, nothing comes remotely near matching its return since March 2021.

| 5-year return (excluding dividends) | |

| Rolls-Royce | 1,040% |

| Babcock Worldwide | 448% |

| BAE Methods | 362% |

| Airtel Africa | 324% |

| Fresnillo | 285% |

In fact, these different companies listed weren’t on the brink throughout Covid, so this explains a number of the outperformance. But there’s no denying that CEO Tufan Erginbilgiç has performed a tremendous job extinguishing the flames on what he referred to as the “burning platform” (ie the previous Rolls-Royce).

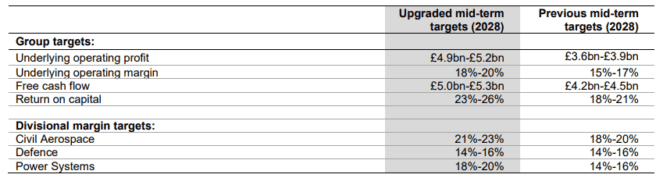

Final yr, the corporate’s underlying working margin reached 17.3%, up from 10.3% in 2023. Keep in mind the unique goal again in 2023 was for an working margin 13%-15% by 2027. So it has obliterated that aim two years early!

In the meantime, free money circulate got here in at £3.27bn, up from £1.26bn in 2023. And the steadiness sheet is much much less of a priority nowadays, with gross debt lowered from £3.6bn to £2.8bn final yr.

In a present of confidence in its monetary future, Rolls-Royce introduced a large multi-year share buyback programme, totalling £7bn-£9bn from 2026 to 2028.

Lastly, the mid-term targets had been upgraded (but once more).

Optionality

I first purchased Rolls-Royce shares in mid-2023 at 149p, then added once more in 2024 at 475p and final yr at 624p. The factor that attracted me was that the engineering agency appeared to have a number of avenues of development. Usually referred to as optionality, that is one thing I search for in investments.

At its core, Rolls’ Civil Aerospace division ought to profit from the rise of long-haul journey. Aircraft maker Airbus initiatives a necessity for 9,170 new widebody plane over the subsequent 20 years, together with each passenger planes and freighters.

In the meantime, large army price range hikes throughout Europe ought to bolster the Defence unit. Final yr, Rolls-Royce secured profitable aftermarket contracts value greater than £1.5bn with the Ministry of Defence and the US Division of Conflict.

Then additional on the market are small modular reactors (SMRs), which can be vital for nations aiming to succeed in internet zero targets. The corporate’s distinctive nuclear capabilities makes it well-placed to change into a worldwide chief on this large rising market.

One space I underestimated was the Energy Methods division, which is rising strongly attributable to hovering energy technology demand pushed by AI information centres.

Purchase extra shares?

So I’m very happy with what I see financially and operationally right here. However what concerning the valuation?

Sadly, the ahead price-to-earnings ratio is 36. Right here, I feel the inventory is priced for perfection. However with warfare raging within the Center East, flights being diverted, and world provide chains already strained, we’re sadly not residing in an ideal world.

For me then, I see higher alternatives within the FTSE 100. But when Rolls-Royce retains dipping, I’ll reassess.