{kind=link}

Picture supply: Getty Photographs

The FTSE 100 fell 1.3% immediately (26 March), so not many shares moved upwards. Because of this, Subsequent (LSE:NXT) stood out like a beacon after it rose 5.2% to 12,665p.

This can come as a aid to shareholders, because the inventory was down 12% 12 months thus far earlier than immediately’s leap. So, what happy the market immediately?

Distinctive outcomes

The catalyst for immediately’s rise was the clothes and residential retailer’s annual outcomes for the monetary 12 months ending January 2026. And as is commonly the best way with Subsequent, it defied the doom and gloom on the market within the long-struggling UK retail sector.

Full-year gross sales had been up 10.8% to £7bn, with 7% progress within the UK and 35% abroad. These figures had been far increased than the unique steering given virtually a 12 months in the past (for five% gross sales progress).

In the meantime, pre-tax revenue elevated 14.5% to £1.16bn, whereas earnings per share jumped 17%. The enterprise generated £1.1bn in free money movement, which was distinctive. It returned £839m to shareholders through dividends, share buybacks, and different strategies.

Nevertheless, whereas gross sales within the first eight weeks of this 12 months had been promising, administration is cautious as a result of warfare within the Center East. It expects full-year gross sales to rise 4.5%, with pre-tax revenue edging up by the identical quantity to £1.21bn.

But when the disruption drags on for longer than three months, CEO Simon Wolfson warned Subsequent must increase costs “within the order of 1% to 2% most“. However then doubtlessly extra, relying on value inflation.

Transferring ahead then, the danger is that inflation-weary consumers rapidly tighten their belts, impacting gross sales progress.

Three issues

Is Subsequent inventory price contemplating for long-term buyers? Nicely, I feel to reply that, there are three fundamental issues: the standard of the enterprise, future progress alternatives, and the valuation.

When it comes to high quality, I feel Subsequent ranks up there with the easiest. Again in September, I referred to it because the “cream of the crop” amongst UK retailers, and final 12 months’s outcomes present why.

To present an instance, take into account this quote from the report: “Each exercise we undertake — from new warehouses and advertising campaigns to the launch of latest manufacturers — should be assessed when it comes to profitability and return on funding. We don’t take pleasure in tasks that some may suppose are ‘strategic’, however provide little hope of excessive returns or wholesome margins.”

Sounds easy, in fact. However because of world-class administration and execution, Subsequent really walks the walks, in addition to delivering the speak. Not many retailers do.

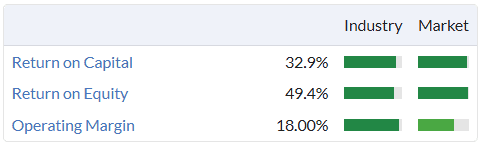

That is mirrored in distinctive high quality metrics.

As for future progress, nicely, I feel Subsequent has barely scratched the floor of the long-term abroad alternative. Worldwide on-line gross sales reached £1.3bn final 12 months, which is a drop within the ocean for the worldwide market.

For instance, it’s focusing on capital-light gross sales enlargement in Asia and the US through on-line aggregator platforms. And given the stagnant UK financial system, it will change into extra essential transferring ahead.

What about valuation? Nicely, shock shock, this high quality inventory isn’t low-cost at round 16 occasions ahead earnings (above the 10-year common of 13.5).

However Subsequent has a strict valuation threshold for getting again its personal shares, and that’s at present £131. With the inventory at £126, I due to this fact suppose it’s price contemplating, particularly on any Center East-related dips.