{kind=link}

Picture supply: Getty Photos

Nvidia inventory’s arguably higher worth than many buyers realise. At $211, it trades at 23.5 occasions ahead earnings, with that a number of falling to 13.1 occasions by fiscal 2029 and simply 11.2 occasions by 2031. Superior Micro Units is pricier at 75 occasions this 12 months’s forecast earnings, although that drops to 16.8 occasions by 2030.

These are the 2 names that dominate the marketplace for AI accelerators — the chips doing the heavy lifting on the planet’s knowledge centres — arguably aside from Google‘s TPUs, that are primarily used in-house.

However there’s a 3rd identify I’ve been watching: Cerebras Programs (NASDAQ:CBRS).

The scary bit first

On right this moment’s numbers, Cerebras appears to be like wildly costly. The corporate’s anticipated to lose $0.97 per share this 12 months, and the inventory trades at 56 occasions forecast gross sales. Nvidia, for reference, is on 13 occasions.

I admire figures like these can look scary. However projecting valuations years into the longer term — and shopping for earlier than the market catches up — is how the perfect buyers make investments. It isn’t only a hunch, it’s about forecasting.

Analysts anticipate Cerebras’ earnings to blow up: $5.84 per share in 2028, $11.54 in 2029, and $16.18 in 2030. At right this moment’s $215 share value, meaning the price-to-earnings (P/E) ratio falls from 36.8 occasions in 2028 to 18.6 occasions in 2029 and 13.3 occasions in 2030.

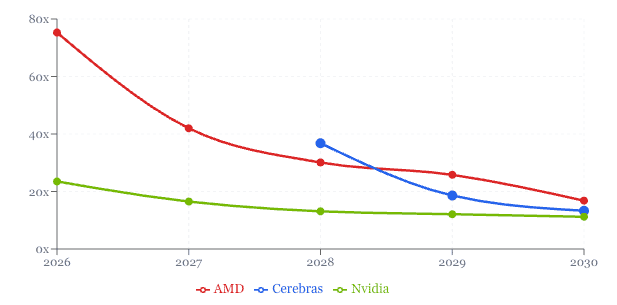

Examine that with AMD at 25.8 occasions 2029 earnings and 16.8 occasions 2030 earnings. On these forecasts, Cerebras turns into cheaper than AMD from 2029 — and by 2030 it’s inside touching distance of Nvidia. This is only one metric, but it surely tells us loads.

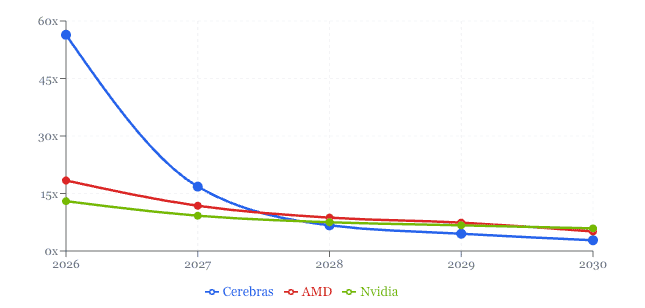

The value-to-sales image is much more putting. Income’s forecast to surge from $863m this 12 months to $17.5bn in 2030, dragging the a number of from 56 occasions down to simply 2.8 occasions — beneath each Nvidia (5.9) and AMD (5.1) by the top of the last decade.

Why I believe it could actually ship

There’s a story behind the numbers — there all the time is. Cerebras’ wafer-scale chips have carved out a real lead in AI inference — really operating fashions, quite than coaching them — routinely serving tokens many occasions sooner than GPU-based rivals.

As AI spending shifts from constructing fashions to deploying them at scale, that inference lead is precisely the place the expansion is anticipated to come back from.

The important thing threat

Right here’s the catch, and it’s an enormous one: each a kind of falling multiples is primarily based on development that hasn’t occurred but. Cerebras must develop income roughly 20-fold in 4 years, swing from losses to $16 in earnings per share, and execute flawlessly in opposition to two of the best-run corporations in semiconductors.

What’s extra, solely a handful of analysts mannequin past 2028, so the additional out we glance, the shakier the bottom. If execution slips, the a number of by no means falls — and right this moment’s 56 occasions gross sales would look very costly certainly.

That stated, I consider it’s a inventory buyers ought to contemplate. AI isn’t going away and I consider this {hardware} shall be integral for many years to come back.

Do you have to make investments £5,000 in Cerebras Programs Inc – Class A proper now?

When investing professional Mark Rogers and his crew have a inventory tip, it could actually pay to hear. In any case, the flagship Twelfth Magpie Share Advisor publication he has run for almost a decade has offered 1000’s of paying members with high inventory suggestions from the UK and US markets.

And proper now, Mark thinks there are 6 standout shares that buyers ought to contemplate shopping for. Wish to see if Cerebras Programs Inc – Class A made the record?

James Fox has place in Alphabet, Cerebras Programs and Nvidia.