{kind=link}

Picture supply: Getty Pictures

Greggs’ (LSE: GRG) shares have been caught beneath 1,800p for over a 12 months now. That’s left many traders, together with me, questioning if there’s any hope of restoration. Ought to we hold holding on – or is it time to promote and chase higher alternatives elsewhere?

To reply that query, I want to determine if it is a momentary hiccup or a extra basic downside. So I’ve been digging into the most recent outcomes and analyst views to get a clearer image.

Let’s see if we will establish the place precisely issues went mistaken for one of many UK’s most beloved bakers.

What’s behind the weak efficiency?

The simplest method to have a look at that is that Greggs is feeling the squeeze from the cost-of-living disaster. Households have been tightening their belts, which has damage like‑for‑like gross sales development and product combine.

Regardless that whole gross sales grew 6.8% to £2.15bn in 2025, pretax revenue fell 18% to £167.4m, with underlying working margins dropping from 9.7% to eight.7%.

Rising wages, vitality and enter prices have compounded the issue, narrowing margins whilst gross sales have grown. As revenue development slowed after which turned detrimental, the valuation premium that Greggs as soon as loved collapsed. The shares now commerce shut to 5‑12 months lows.

What’s extra, Greggs has grow to be probably the most shorted UK shares, reflecting deep scepticism a few close to‑time period earnings restoration. Administration has mentioned any revenue enchancment in 2026 is “contingent on a restoration within the client backdrop“, tying the inventory’s destiny intently to the broader UK financial system.

But when the financial system does flip, might Greggs bounce again strongly?

The (tentative) bull case

There are some encouraging indicators. Early 2026 buying and selling confirmed higher like‑for‑like gross sales versus the prior 12 months, and full‑12 months steering was maintained slightly than reduce.

Capital expenditure is predicted to fall from £287.5m in 2025 to about £200m in 2026, after which £150m-£170m from 2027, liberating up money for additional retailer growth. Plus, the 4.3% yield provides revenue attraction.

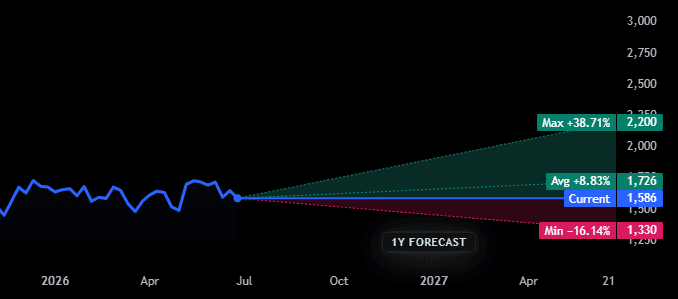

The shares additionally look low-cost on paper. They commerce on roughly 13 occasions ahead earnings for 2026, effectively beneath Greggs’ 10‑12 months common. Analyst value targets common round 1,850p, with a spread from 1,330p-2,200p, implying average development potential if the restoration takes maintain.

However right here’s the catch: any restoration stays tightly linked to the UK client. If the price‑of‑residing disaster persists, it’s unlikely we’ll see significant enchancment in Greggs’ short-term earnings.

So is that this a inventory to carry or fold?

My take

For affected person shareholders like me, there’s an opportunity of constructive returns over the subsequent 3-4 years if client confidence recovers. The struggling excessive avenue baker would possibly nonetheless shock us all, however the bull case is weakening by the day.

Realistically, it’s changing into tougher to see a compelling alternative for brand spanking new traders within the present atmosphere. The dangers look elevated, and the expansion story is now not what it as soon as was.

The actual query is, how for much longer are you keen to attend for Greggs to enact a significant turnaround?

For these chasing shorter‑time period development, I feel the capital may very well be used to focus on higher returns elsewhere. However for affected person worth traders proud of average revenue, it’s nonetheless value a glance.

What revenue inventory can we like higher than Greggs Plc proper now?

Certainly one of our Share Advisor analysts has simply launched a model new inventory report that we expect is a must-read for any investor trying to try to generate potential revenue.

And the perfect bit is you can see if for your self, proper now, completely freed from cost!

No jargon. No onerous promote. Only a clear take a look at an revenue share we expect is value your time.

Mark Hartley owns shares in Greggs.