{kind=link}

Picture supply: Getty Photographs

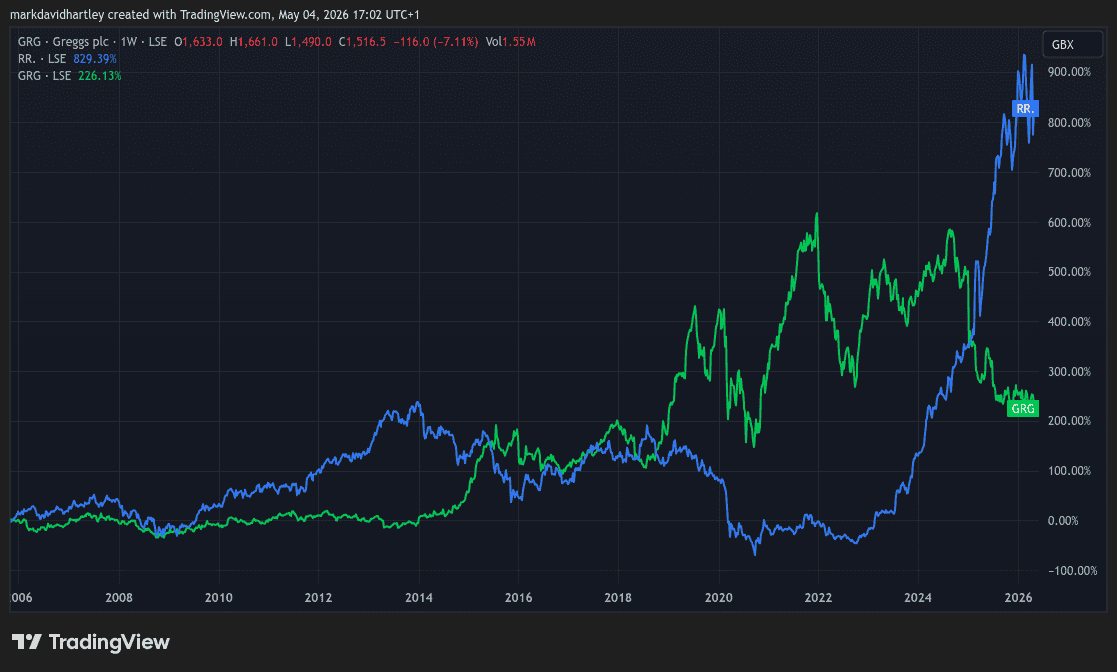

At the moment buying and selling round £15 every, Greggs (LSE: GRG) shares have misplaced greater than half their worth since their 2022 excessive above £33.

It’s a stunning comparability to the promising progress inventory it as soon as was within the late 20-teens. And that’s precisely why it carefully mirrors the worth exercise of Rolls-Royce between 2010 and 2020.

So might Greggs do a full 180 and rack up exponential beneficial properties within the coming 5 years?

Let’s take a better look.

Macro challenges

The parallels between Greggs at the moment and Rolls-Royce in prior years run deeper than simply the share value.

In each circumstances, sharp downturns have been pushed largely by exterior components. In Rolls’ case, the Covid-19 pandemic grounded world air journey. For Greggs, shifting client habits and wage hikes have hit income arduous.

However we are able to’t attribute Rolls’ success purely to recovering air journey, in any other case all airways would have comparable fortunes. The function of CEO Tufan Erginbilgiç within the restoration can’t be overstated, which is the place Greggs comes into query.

Can Gregg’s CEO Roisin Currie, appointed in 2022, assist the bakery enact a Rolls-like restoration?

Why a Greggs restoration is believable

A number of components play into the narrative of a robust restoration for Greggs. Most notably, it nonetheless has a robust underlying model and money movement.

It’s seen as a number one ‘worth meals‑to‑go’ model, with resilient like‑for‑like gross sales, and a pipeline of retailer openings and new‑venue codecs (rail, forecourts, supermarkets).

After its sharp fall from 2021 highs, analysts now describe it as ‘low-cost’ relative to earnings and money technology. The present value is barely 12 occasions estimated future earnings.

That’s enticing for a client‑defensive, asset‑mild enterprise. With prices falling, administration now targets a return on capital employed (ROCE) restoration of round 20%. So even a modest margin enchancment might re‑fee the shares.

Which means the expansion narrative of the 20-teens might return in full pressure – if exterior points ease.

However will or not it’s a Rolls-like restoration?

Whereas I’m optimistic about Greggs, I’m additionally real looking. Rolls’ 1,000%+ rally got here from a leveraged steadiness sheet turnaround, double‑digit margin growth, and in depth authorities defence spending.

Greggs is totally different in that it’s a smaller, extra cyclical, aggressive client‑retail inventory. It doesn’t exhibit fairly the identical structural leverage and explosive potential.

Add to that ongoing challenges just like the cost-of-living disaster, weather-sensitive foot visitors, and evolving consuming habits, and it faces a tricky future.

I believe it’s cheap to count on progress within the 300%-400% vary over the approaching 5 years if circumstances enhance and it caters to altering habits.

But it surely’s extremely unlikely that any FTSE inventory will match Rolls’ once-in-a-decade efficiency.

The underside line

Arguably the UK’s hottest excessive avenue bakery chain, Gregg’s has grown aggressively since 2020. Between 2020 and 2025, it elevated its retailer depend from round 2,000 to over 2,700.

However the speedy growth might have been untimely. After the Labour authorities launched budgetary modifications in October 2024, the corporate was confronted with the specter of rising prices.

And but regardless of these ongoing dangers, it’s managed to take care of a wholesome steadiness sheet. Shrinking margins are a priority however rising money movement and a lovely valuation trace at restoration potential.

The longer term could also be unsure, however for worth traders optimistic concerning the UK economic system, Greggs is a compelling possibility to think about.