{kind=link}

Picture supply: Getty Pictures

Efficiently figuring out worth shares is key to worthwhile investing. However the place to begin? Most analysts take a look at future money movement forecasts to give you a valuation in immediately’s cash. That is, nonetheless, very labour-intensive. And what when you haven’t obtained the time to carry out these kinds of calculations?

Thankfully, there’s a comparatively fast option to try to establish low-cost shares. And I’ve used it to seek out one instance of what I imagine is a bargain-basement worth inventory.

A fast overview

As its identify suggests, the price-to-earnings (P/E) ratio measures an organization’s share worth relative to its revenue. In easy phrases, it defines how a lot traders are ready to pay for £1 of earnings. In principle, the decrease the quantity, the cheaper the shares.

Nevertheless, it’s vital to use a little bit of judgement when utilizing the P/E ratio. A low determine may indicate that traders are involved concerning the firm’s prospects. For instance, earnings is likely to be going within the incorrect route. And ratios will differ throughout completely different industries. Capital-intensive sectors are likely to have decrease valuation multiples.

Out of trend

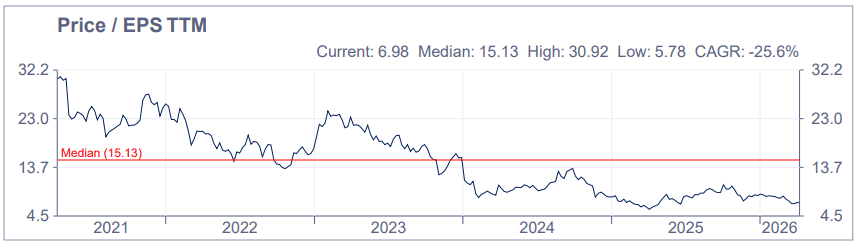

However I feel it is sensible to trace a inventory’s P/E ratio over time. And that’s what makes me assume that shares of JD Sports activities Vogue (LSE:JD.) provide large worth in the mean time (9 April).

Primarily based on forecast earnings per share (EPS) of 11.37p for the yr ended 31 January 2026 (FY26), the inventory’s buying and selling on a particularly engaging 6.5 instances earnings. The five-year common (median) is 15.1.

And if analysts’ forecasts show to be correct, the sports activities retailer’s ahead P/E ratios are 6.5 (FY27) and 5.9 (FY28).

A difficult market

However keep in mind what I mentioned earlier a few low quantity being a potential warning signal? Properly, it may apply right here.

The group’s been rising by shopping for new shops however its like-for-like (LFL) gross sales have been falling. Throughout the 48 weeks to three January, they have been down 2.1% in comparison with the identical interval a yr earlier. The worst-performing area was the UK with a reported 4% drop.

It’s estimated that Nike’s merchandise account for round half of JD Sports activities’ gross sales. However the American sportswear large’s been struggling recently. There are some early indicators that it’s recovering however it’s nonetheless not out of the woods.

As well as, issues have been raised that the British retailer’s core demographic of 18-to-24-year-olds are seeing their residing requirements affected by synthetic intelligence options changing entry-level jobs.

Not all dangerous

Regardless of these challenges, I nonetheless assume the group’s shares are in cut price territory.

Over 60% of the group’s shops at the moment are in North America, that are performing higher than its European ones. Additionally, it’s not completely reliant on Nike. Different manufacturers, Adidas being essentially the most notable one, are doing very nicely in the mean time. This yr’s soccer World Cup may additionally raise gross sales.

And JD Sports activities stays money generative. With free money movement of over £400m in FY26, it ought to have the scope to refresh a few of its shops in an try to get its LFL gross sales rising once more. The consensus of these analysts which have modelled the group’s money movement potential reckon the inventory’s 26% undervalued.

Weighing every little thing up, I imagine JD Sports activities is nicely value contemplating by traders immediately.