{kind=link}

Picture supply: Getty Photos

When shares include 9% dividend yields, it’s nearly all the time an indication traders are involved about one thing. However the market isn’t all the time proper – and when it’s not, they are often large alternatives.

Each the FTSE 100 and the S&P 500 have shares with eye-catching yields proper now. And traders searching for long-term passive revenue ought to take a more in-depth have a look at each.

LyondellBasell Industries

At 9.5%, LydonellBasell Industries (NYSE:LYB) has the best dividend yield within the S&P 500. And it’s a traditional one for traders – the yield is up as a result of the inventory is down, so is the dividend protected?

The agency is a chemical substances enterprise that’s in a downturn. Weak demand resulting from faltering industrial exercise has compressed margins, however the greater situation has been provide competitors from China.

Over the past 12 months, the corporate’s free money move has been nowhere close to sufficient to cowl its dividend. And which means there’s an actual danger of decrease distributions – and the market is aware of it.

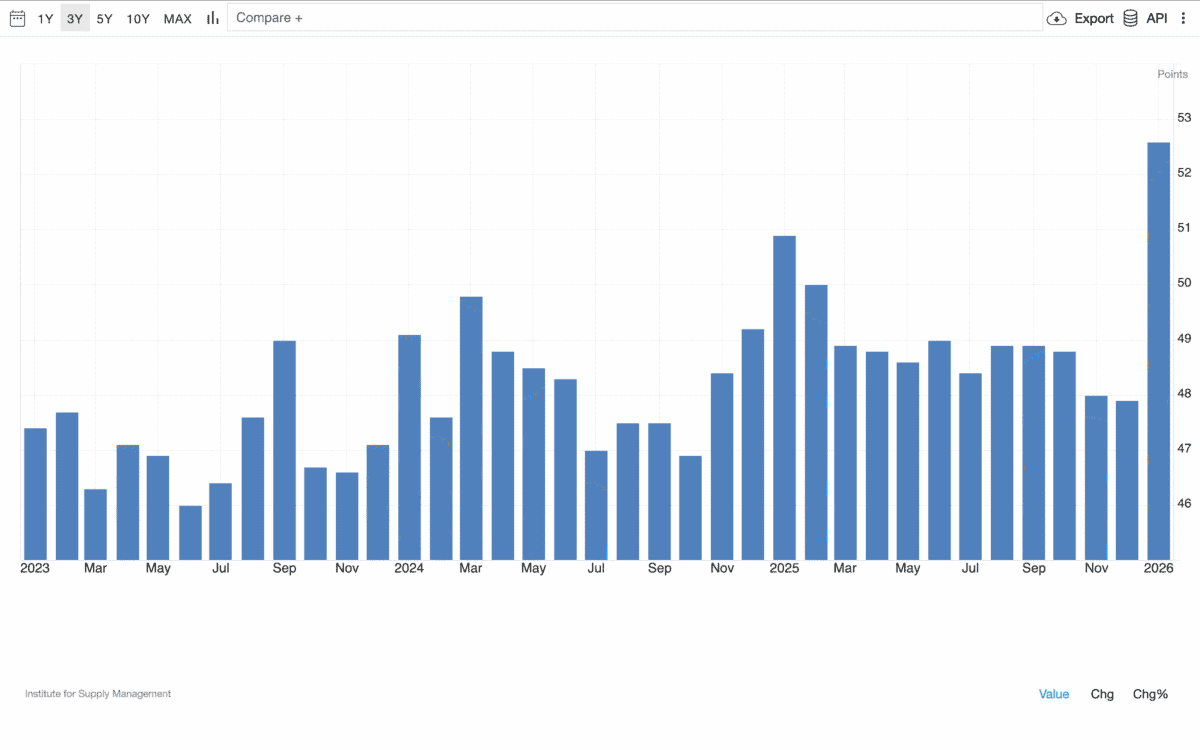

A dividend lower isn’t assured although, and there are causes for positivity. One is that there are indicators of a restoration in US industrial exercise coming from January’s ISM Manufacturing PMI knowledge.

Supply: Buying and selling Economics

The determine got here in at 52.6, which is its highest degree in three years and a powerful signal of progress. And so as to add further weight to this, the availability facet of the equation is beginning to enhance in China.

Tax coverage has really compelled a few of China’s much less environment friendly operations to close down, lowering competitors. Given this, I feel the 9.5% dividend yield is certainly value a more in-depth look.

Admiral

From the FTSE 100, Admiral (LSE:ADM) is a really totally different case. The £2.36 per share the agency returned in 2025 is an 8.3% yield at as we speak’s costs, however that’s undoubtedly going to be decrease in 2026.

The corporate has introduced a shift in its capital allocation coverage. As a substitute of issuing new shares to fund worker compensation, it’s going to make use of the particular dividend to finance this.

That’s going to imply money returns are decrease going ahead. But it surely doesn’t symbolize a way by which the enterprise is basically any worse – in reality, it is perhaps the alternative.

Shopping for its personal shares as a substitute of paying dividends is perhaps extra tax-efficient for traders. And the corporate’s core energy is the profitability of its underwriting, which isn’t affected by the change.

One danger is that the UK automotive insurance coverage business is beneath stress proper now. Greater restore costs and decrease premiums are set to weigh on margins, which is why analysts have been downgrading the inventory.

They is perhaps proper, however I feel Admiral is in a greater place to deal with a downturn than most. And whereas revenue traders would possibly wish to look elsewhere, I’ve began shopping for the inventory in my ISA.

Excessive yields, excessive danger?

Warren Buffett’s level that traders pay a excessive worth for a cheery consensus is completely true of dividend shares. Excessive yields nearly all the time mirror concern in regards to the underlying enterprise.

Typically although, the priority might be unjustified resulting from a short-term situation that the market is unable to see previous. And when that occurs, traders can discover uncommon and profitable funding alternatives.