{kind=link}

Picture supply: Getty Photos

Shares in FTSE 100 knowledge firm RELX (LSE: REL) have been completely crushed just lately. Amid investor considerations over the specter of synthetic intelligence (AI) expertise from the likes of Anthropic and OpenAI, the inventory has fallen round 50% during the last six months.

Might we be a significant discount right here? Let’s check out at present’s full-year 2025 outcomes for clues.

Stable efficiency in 2025

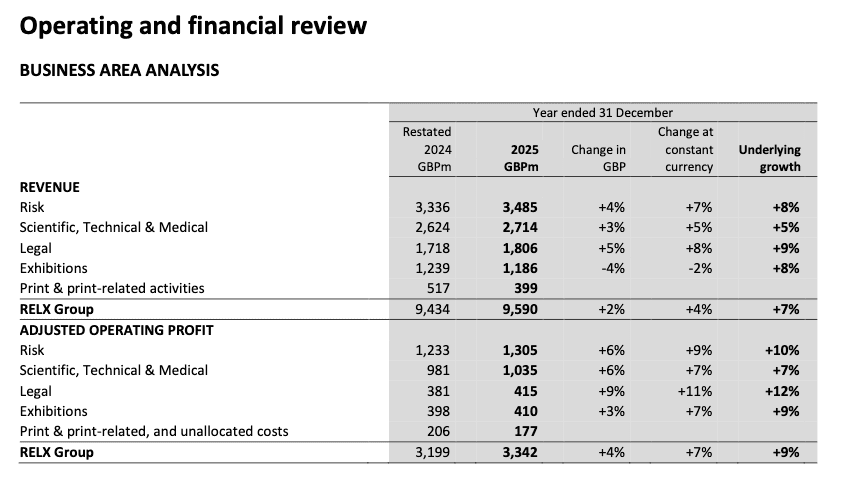

RELX’s outcomes for 2025 have been stable. For the 12 months:

- Income was up 7% on an underlying foundation to £9,590m

- Adjusted working revenue was up 9% on an underlying foundation to £3,342m

- Adjusted earnings per share (EPS) have been up 10% at fixed forex to 128.5p

The desk under exhibits a breakdown of efficiency within the firm’s completely different divisions. Its greatest phase, Danger, carried out nicely, delivering 8% development, as did Authorized, with 9% development.

Upbeat steerage for 2026

After all, that is all backward wanting and the specter of AI is a future situation. So, what did the corporate say in regards to the future?

Properly, for 2026, it highlighted “constructive momentum throughout the group”, and expectations of “one other 12 months of sturdy underlying development in income and adjusted working revenue.”

In the meantime, for each the Danger and Authorized segments in 2026, the corporate mentioned: “We count on continued sturdy underlying income development with underlying adjusted working revenue development exceeding underlying income development.”

On the subject of AI, CEO Erik Engstrom added that it’s enabling it so as to add extra worth for patrons, “as we embed extra performance in our merchandise, and to develop and launch merchandise at a quicker tempo, whereas persevering with to handle value development under income development”. It is going to “stay a key driver of buyer worth and development in our enterprise for a few years to come back.”

All of this means that the corporate doesn’t see AI as a lot of a menace within the close to time period. If something, administration seems to consider that AI will assist to drive development.

It’s value noting that the corporate elevated its dividend by 7% to 67.5p per share. Wouldn’t it have executed that if it noticed AI as an existential threat?

A FTSE 100 worth play?

So, are we a discount within the Footsie right here? I feel so.

For a begin, the corporate’s forward-looking price-to-earnings (P/E) is simply 14. That’s low for an information firm rising at a wholesome fee.

Secondly, with a relative energy index (RSI) of simply 17, the inventory seems massively oversold. The RSI is a technical evaluation indicator that measures the magnitude of latest share worth actions (a studying below 30 signifies oversold).

Third, the agency mentioned that it plans to purchase again £2,250m value of inventory in 2026 (versus £1,500m in 2025). That implies administration sees the inventory as undervalued.

After all, AI does add uncertainty as a result of there are some components of its enterprise that might be disrupted by the likes of Anthropic and OpenAI. An instance is its Lexis+ platform, which permits attorneys to draft briefs.

General although, I like the danger/reward proposition at present ranges. I feel this inventory is value a better look proper now.