{kind=link}

Picture supply: Getty Pictures

Palantir Applied sciences (NASDAQ: PLTR) inventory has a behavior of exploding larger after an earnings stories. This has seen it rise by a mind-boggling 780% in two years!

The AI software program agency stories Q2 earnings on 4 August. Ought to I snap up some shares earlier than this occasion?

Booming AI enterprise

Palantir develops software program that permits organisations to analyse and act on giant volumes of information. Its large buyer base consists of the likes of the US Military, CIA, NHS England, Airbus, and Ferrari.

Not too long ago, it has been the corporate’s Synthetic Intelligence Platform (AIP) that has supercharged the enterprise and share worth. AIP integrates giant language fashions (LLMs) and different AI instruments straight with an organisation’s personal knowledge and workflows.

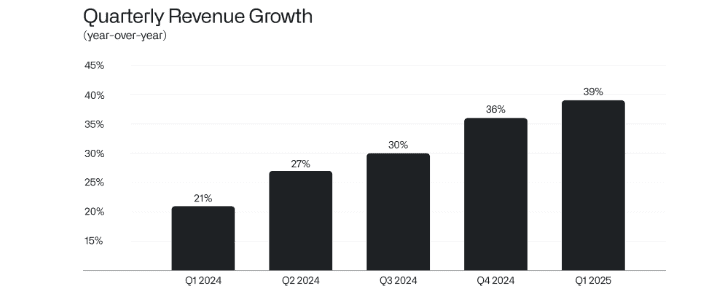

The surge in contracts signed for AIP has been most pronounced throughout the pond. In Q1, US income jumped 55% yr on yr to $628m, with US industrial income rocketing 71%. Total income elevated 39% to $884m.

Impressively, Palantir closed 139 offers of not less than $1m, 51 of not less than $5m, and 31 offers of $10m or extra in the course of the quarter. Adjusted free money circulate got here in at $370m, good for a really wholesome a 42% margin.

The primary motive for the inventory’s unbelievable ascent skywards is that the quarterly charges of income development have been accelerating. At any time when this occurs, buyers understandably get very excited (particularly when it’s been pushed by AI).

Co-founder and CEO Alex Karp commented: “It is a stage of surging and ferocious development that will be spectacular for an organization a tenth of our measurement. At this scale, nonetheless, our ascent is, we imagine, unparalleled.”

Have I missed the boat?

Clearly that is all very spectacular stuff. However every time I take a look at Palantir, I can’t assist feeling pangs of remorse. That’s as a result of I used to be kicking the tyres on this inventory a few years in the past when it was at $9. However I by no means invested.

Now, I can’t assist feeling like I’ve missed the boat, as Palantir has an enormous $373bn market cap. This makes it the Twenty first-largest firm within the US, forward of Coca-Cola, McDonald’s, and Financial institution of America.

Furthermore, it’s buying and selling at 126 instances gross sales, which simply appears ridiculous to me. Why so? As a result of Wall Avenue presently has round 30%-35% development pencilled in for the following three years. Whereas that’s undoubtedly spectacular, it doesn’t justify 126 instances gross sales, in my view.

At this valuation, I see a variety of threat. If AI spending instantly slows, or earnings are available barely gentle, the inventory might unload closely.

Additionally, a variety of the expansion Palantir is seeing proper now pertains to the US, and the CEO has been extremely important of Europe not embracing AI. He reportedly stated that it’s “like individuals have given up“, when talking about Europe’s AI ambitions.

Due to this fact, a lot of Palantir’s development rests on the US (and pockets elsewhere, like Saudi Arabia). A US recession sparked by tariffs is subsequently a near-term threat to development.

My transfer

My view right here is that Palantir is a world-class software program firm with an infinite long-term alternative in AI. Nonetheless, the inventory is buying and selling far too expensively for me to really feel comfy investing at this time.

If there was a serious pullback within the share worth, nonetheless, that will be a unique matter.