{kind=link}

Snap Inc., the guardian firm of Snapchat, has printed its Q1 2026 earnings report, which exhibits a continued decline in utilization in its key markets, although its advert enterprise stays regular.

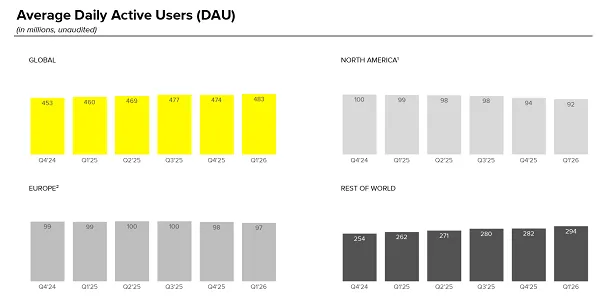

First off, on customers. Snapchat added 9 million extra every day lively customers over its This fall rely, taking it to 483 million complete DAU. That’s a major end result, contemplating that Snapchat misplaced 3 million customers, quarter-over-quarter, within the final reporting interval.

The topline progress, nevertheless, isn’t reflective of Snap’s key markets.

Within the North American market, the place Snapchat generates the vast majority of the platform’s revenue, the app’s every day utilization declined by one other 2 million, sliding to 92 million DAU, whereas within the EU, Snap utilization shrunk by 1,000,000 individuals versus the earlier quarter.

In different phrases, all of Snap’s progress is coming from areas the place it’s nonetheless growing its enterprise instruments, and doesn’t generate as a lot revenue.

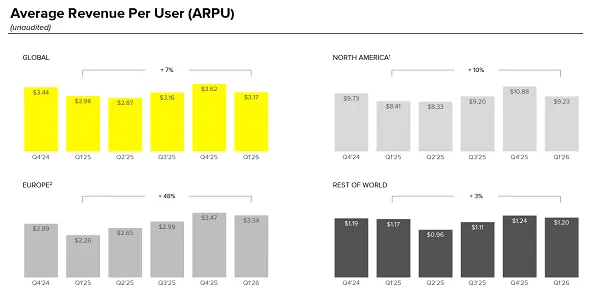

Snapchat is enhancing on this entrance, however because the above chart exhibits, Snap continues to be producing considerably much less income per person within the markets the place it’s seeing progress.

So whereas general progress is a constructive word, it’s nonetheless considerably problematic for Snap, except the platform can discover a technique to generate extra revenue from these customers.

One other key problem for Snap is the growing push for elevated age restrictions on social media use. Many areas wish to observe Australia’s lead in implementing bans for customers beneath the age of 16, so as to restrict the damaging impacts of social media use and publicity.

That might damage Snap extra considerably than different platforms, given its reputation amongst youthful audiences.

In February, Snapchat reported that Australia’s teen ban had pressured it to lock or disable the accounts of 415,000 customers. That’s in a nation with a inhabitants of round 27 million, so it’s not laborious to think about the expanded affect teen bans would have in, say, Germany (84 million inhabitants), the U.Okay. (69 million) or Spain (49 million), all of which are additionally contemplating teen social media bans.

The cumulative impact, then, might have a serious affect on Snap’s broader progress plans, which is one other vital danger issue for the app.

Snapchat additionally reported that month-to-month lively utilization elevated to 956 million general, up from 946 million in This fall.

On the income entrance, Snapchat introduced in $1.53 million for the quarter, which represents a 12% year-over-year enhance.

Snap stated that Sponsored Snaps drove robust efficiency features, whereas its Dynamic Product Advertisements income grew greater than 30% year-over-year, and noticed specific progress amongst SMB prospects.

So Snap is diversifying its advert income, and driving extra features with a broader vary of manufacturers. Although its progress, at current, is regular, and future growth shall be tied to general utilization to a major diploma.

Basically, Snapchat wants to maximise its enterprise alternatives in additional areas, as a result of its declining utilization within the U.S. and EU will restrict its capability.

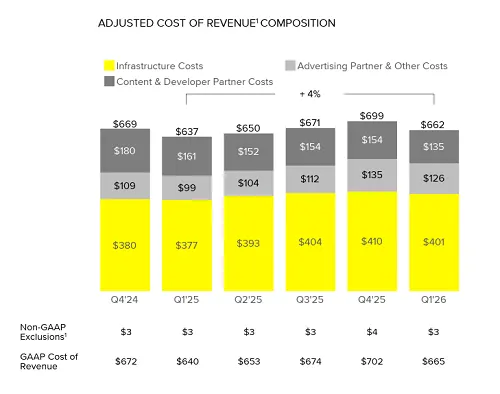

Additionally, its prices stay excessive:

Snapchat has been working to chop prices, and enhance its general viability, because it continues to develop its advertisements enterprise, and construct on its current alternatives.

However the problem is obvious.

Snap CEO Evan Spiegel has known as this a “crucible second” for the app, as it really works to compete with the tech giants, whereas additionally heading off competitors from rising startups seeking to faucet into its core market.

And whereas Snapchat’s progress has basically slowed, and reversed in key markets, it’s nonetheless a key focus app for a lot of customers. The issue for Snapchat is that it doesn’t stay a crucial app as those self same customers shift into older demographics, so its alternative is inherently restricted, which means its market capitalization can also be confined to some extent.

Snap has been attempting to buck this, by discovering new advert alternatives, like advertisements in person DMs, and expanded placements to assist advertisers attain its influential viewers. However that additionally has an higher restrict, and it looks like solely a matter of time earlier than Snap customers begin to complain concerning the inflow of advertisements interrupting their connective expertise.

And Snapchat’s general progress technique define, which it offered to buyers final month, it does seem to be it’s going to be powerful going.

Snapchat continues to be progressing in the direction of the primary aim right here, although as famous, its progress in its main markets goes backwards, so that won’t find yourself being as spectacular because the topline determine suggests.

Snapchat’s innovation additionally hasn’t developed rather a lot in recent times, past including Highlight, which it copied from TikTok. And whereas subscription income is rising, Snapchat+ revenue is rarely going to match to its advert consumption.

Which then leaves improved efficiency in driving extra advertiser curiosity, which might turn out to be an issue if customers get sick of so many advertisements.

After which it’s AR glasses, which Snap continues to be seeking to launch this yr.

However Snapchat’s chunky, heavy AR machine seems set to be inferior to Meta’s AI glasses proper off the bat, and even with superior AR performance, I’m undecided that there’s going to be massive shopper demand for the machine.

And if Meta releases its personal AR glasses in 2027, because it has deliberate, I don’t anticipate Snap’s AR wearables to be a giant winner both.

So Evan Spiegel is correct, this actually is a crucible second, with reference to it being a serious take a look at of Snap’s capability to compete. Now, we wait and see what comes subsequent.